Why Payment Processors Hold Funds (and How Service Businesses Can Avoid It)

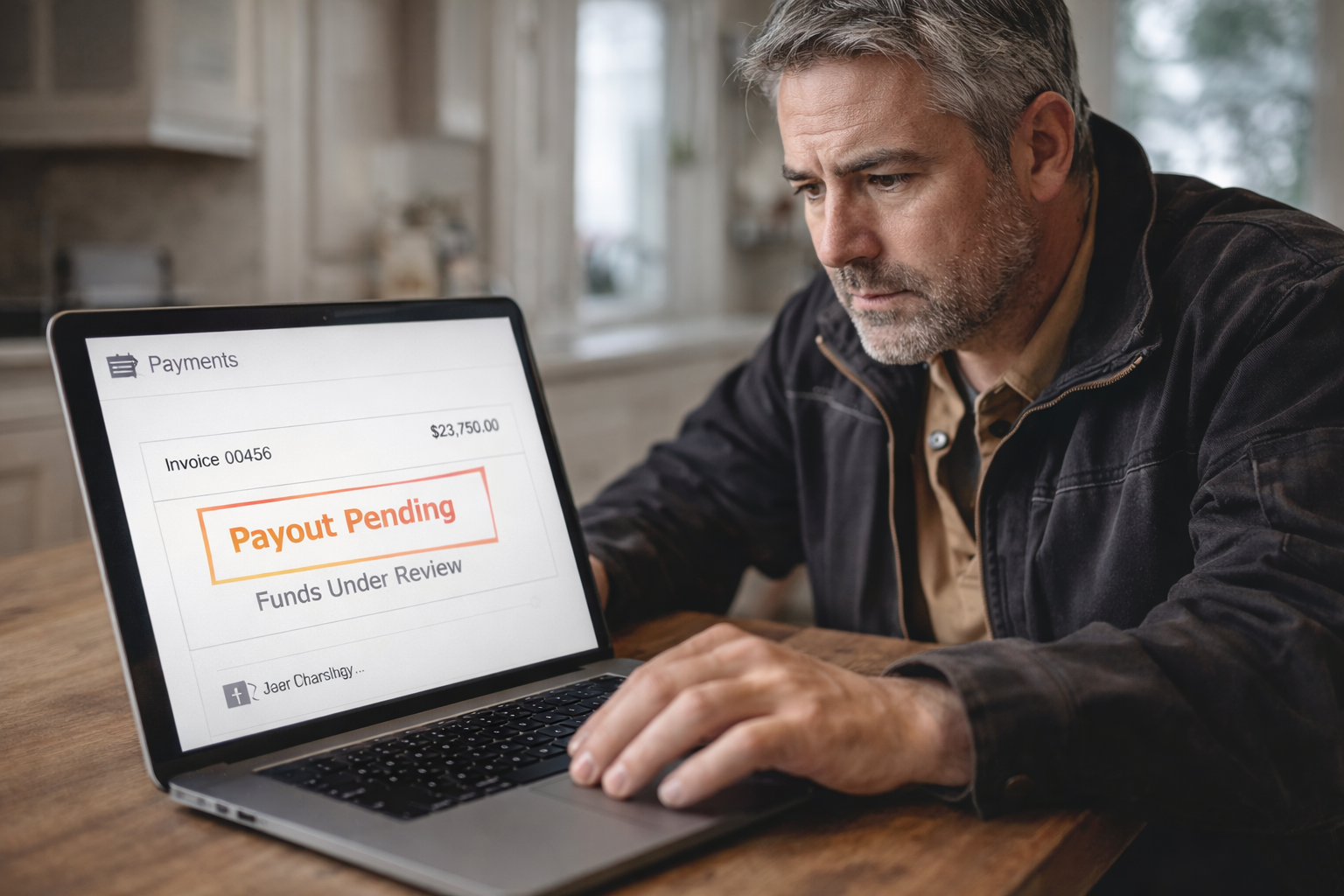

Getting an email from your payment processor saying they’re going to hold 20% of your card sales is a nightmare.

For many service businesses, it happens without warning. One large job, one spike in volume, and suddenly your cash flow is locked up for months.

The best way to avoid this isn’t reacting after the fact. It’s working with a processor that underwrites your business before the storm hits.

If your funds are currently being held, or you’ve been hit with a rolling reserve and need a merchant account built for service-based businesses, you can reach us here:

👉 https://ethicalpaypro.com/contact/

If you want to understand why processors do this and how to prevent it going forward, keep reading.

Why Payment Processors Hold Funds

Payment processors are responsible for managing fraud and chargeback risk at scale. To do that, most rely on automated risk systems that look for activity outside a business’s normal pattern.

For service businesses, the most common triggers are:

- Large ticket sizes compared to historical averages

- Sudden spikes in volume, especially early on

- Extended delivery timelines, typically more than 30 days from the initial deposit

These controls exist to reduce fraud. Unfortunately, they often collide with how legitimate service businesses actually operate.

Why This Hits Service Businesses the Hardest

In blue-collar and service-based work, it’s normal to:

- Take deposits upfront

- Run milestone or progress payments

- Land occasional large or unexpected jobs

- Deliver work 30+ days after the initial deposit

To an automated risk system, that looks dangerous.

To a contractor, it’s just business.

This is why many instant-onboarding processors quietly impose internal limits. A common one is around $5,000 in early card volume.

If that threshold is hit too quickly, automated systems often respond by holding funds, adding a rolling reserve, or freezing payouts while documentation is requested.

The onboarding was instant, but the risk review happens after money starts moving

What We Do Differently

We don’t believe in instant onboarding followed by surprise holds.

Instead, we collect key documentation upfront, including:

- Bank statements

- Prior processing history, when available

- Proof of business existence such as licenses or tax permits

This allows us to confirm the business is legitimate and set realistic expectations for ticket size and volume from the start.

If your average ticket is $2,000 and your high-end jobs run $10,000, that’s established day one.

And if you land a job that’s significantly larger than expected, you don’t lose access to your money.

You submit the invoice, we review it, and in many cases we can approve the transaction within hours, instead of holding funds for months or imposing a rolling reserve.

When Purchasing Cards Trigger Holds

Purchasing cards, or P-cards, are common in service and contracting work. Many businesses only run them once per month, often for large end-of-month invoices.

That pattern alone can confuse automated risk systems.

Here’s a real example.

A service business was processing consistently with a top-tier processor, running approximately $300,000–$400,000 per month in card volume.

They landed a new contract that required end-of-month billing on a purchasing card, with expected monthly charges between $700,000 and $1.2 million.

The first time they ran the card, the transaction was flagged and the funds were immediately held.

Documentation was submitted promptly.

Two weeks later, the funds were still not released.

We boarded this same merchant in under 24 hours, collecting documentation upfront and setting clear expectations around ticket size, billing cadence, and purchasing card usage.

Two weeks later, when they ran their first large purchasing card transaction with us, the payment was funded in under 48 hours.

That funding occurred before their previous processor released the prior month’s held funds.

The difference wasn’t the business, the card, or the customer.

It was when and how the risk was reviewed.

Large transactions don’t need to be risky. They just need to be expected.

What to Do If Your Funds Are Being Held

Fund holds and rolling reserves exist to reduce fraud. But if you are a real service business, you should be able to support your processing with documentation that reflects how you actually operate.

If your processor has frozen funds, added a rolling reserve, or asked for documents only after holding your money, it may be time for a merchant account built for service-based businesses.

You can reach us here to talk through your situation:

👉 https://ethicalpaypro.com/contact/