The Peptide Payment Problem Is Breaking — Here’s What Comes Next

The peptide market has been operating inside a regulatory contradiction for years. That contradiction distorted the science and created a hostile environment for payments.

In September 2023, the FDA pushed a number of peptides into Category 2 (“Bulk Drug Substances That Raise Significant Safety Risks”), effectively freezing any path toward legitimate, scalable commercialization.

Now, that position is starting to unwind.

With the FDA set to bring a group of peptides back under formal review through the Pharmacy Compounding Advisory Committee (PCAC) — with the first meeting scheduled for July 2026 and additional sessions to follow — the downstream effect is obvious:

Payments are about to shift fast.

If you’re selling peptides, expect conditions to improve and start preparing to replace duct-tape payment setups with something more secure.

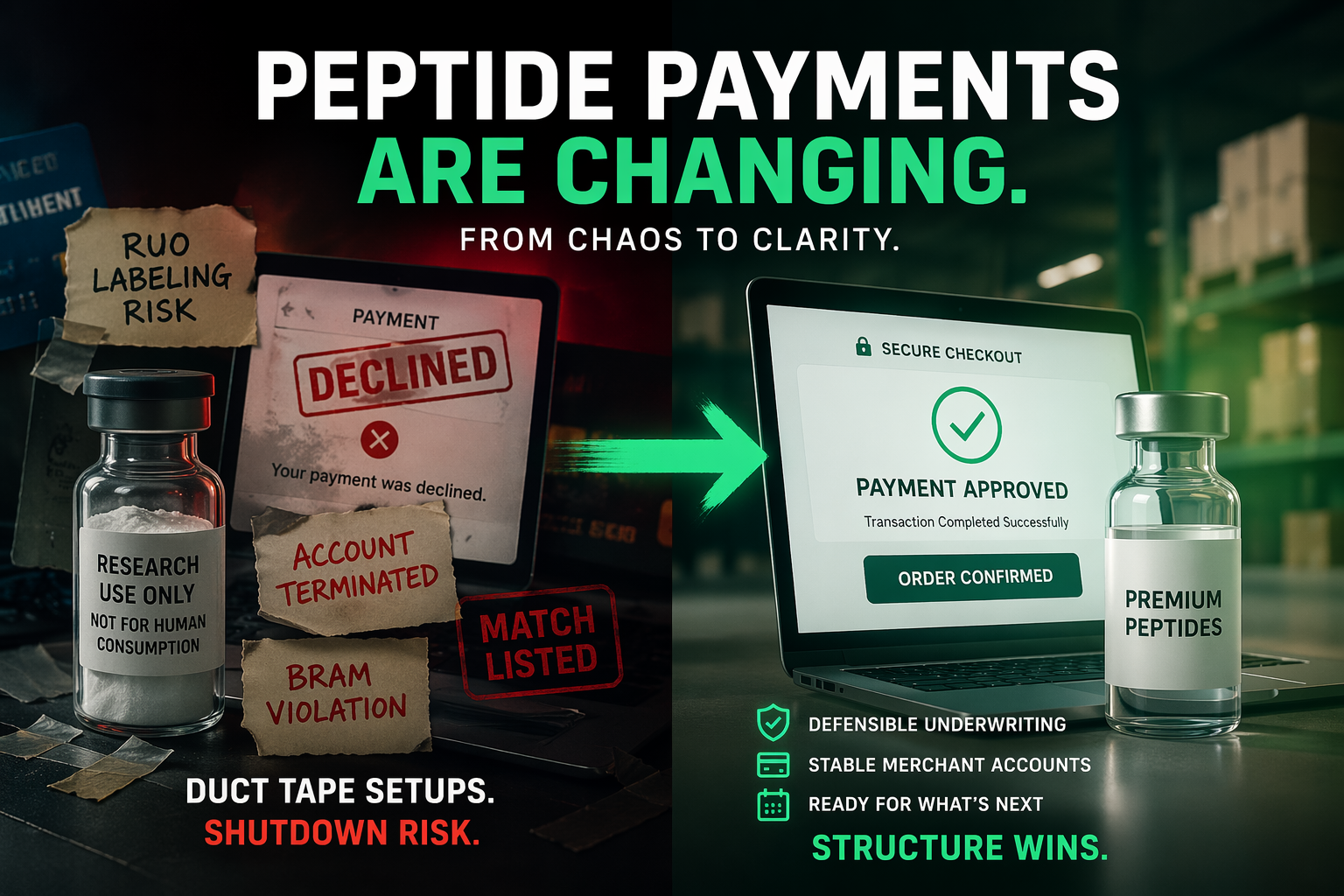

The Current Reality: A Broken Payment Environment

Right now, peptide merchants deal with three bad options:

- Get declined outright by mainstream processors

- Get approved, then shut down midstream

- Hide behind “research use only” (RUO) labeling and hope no one looks too closely

None of these are scalable. All of them carry real risk.

Processors don’t reject peptide merchants because they dislike the category. They reject them because the regulatory framing made underwriting difficult to defend.

You created a situation where:

- The product is widely used by humans

- The labeling says “not for human consumption”

- The marketing often contradicts that label

- The SKU format (single vials, dosing sizes) clearly signals end use

That’s a compliance problem most processors will not touch.

Who Is the Best Payment Processor for Peptide Retailers Right Now?

This is the question every operator asks after getting declined a few times.

Who is the best payment processor for peptide retailers that are not operating through a doctor or compounding pharmacy?

Right now, there isn’t a clean answer.

What exists today:

- processors willing to take the risk short term

- offshore setups with weak stability

- domestic accounts that don’t survive underwriting reviews

Here’s the part most merchants ignore:

Short-term approvals come with long-term consequences.

Those “yes” approvals often lead to:

- BRAM violations tied to prohibited or misclassified activity

- MATCH listings that block you from getting a new merchant account for years

- sudden account terminations with no recovery path

- fund holds or reserves that choke cash flow

These are not edge cases. They are common outcomes in this category.

None of these options are durable.

The core issue is not a lack of processors. The issue is that the regulatory framing made it difficult for any legitimate processor to support the category at scale.

That starts to change as peptides move through formal review beginning in July 2026.

As clarity improves, a small number of processors will step in with:

- structured underwriting

- bank support

- long-term stability

That’s when this question will finally have a real answer.

The RUO Lie Everyone Is Forced to Tell

“Research Use Only” is not a business model. It’s a workaround merchants leaned on because there was no clean way to meet real demand.

The problem:

- Customers are not labs

- Orders are not bulk research quantities

- Packaging looks like direct-to-consumer fulfillment

- Repeat purchase behavior mirrors therapeutic use

Processors see this immediately.

The typical outcome:

- flagged for misrepresentation

- MID terminated

- funds held

- MATCH listing

That sequence shuts most operators down for years.

The Channel That Already Works (But Doesn’t Scale)

Doctors can already prescribe certain peptides through licensed compounding pharmacies when backed by a legitimate medical need.

That channel is:

- compliant

- regulated

- defensible from a payment perspective

It also comes with constraints:

- requires physician access

- higher cost structures

- slower onboarding and fulfillment

- not designed for broad consumer demand

That gap created pressure, and that pressure pushed demand into direct-to-consumer channels using RUO positioning.

The Single-Vial Paradox

If you sell:

- small vial sizes

- direct-to-consumer quantities

- repeat orders

you signal human use behavior.

If you acknowledge human use, you step outside RUO positioning.

That leaves you in a bind:

- tell the truth → non-compliant

- follow RUO → appears misleading

Processors see that conflict and avoid it. It creates underwriting exposure they cannot justify to banks or card networks.

That’s why peptides became a default decline category across many portfolios.

What’s Changing Now

The FDA is pulling certain peptides out of Category 2 and moving them into formal evaluation through PCAC beginning July 2026.

That shift opens the door for payments.

1. Defensible Underwriting Becomes Possible

Processors can now point to:

- active regulatory review starting July 2026

- defined evaluation pathways

- reduced ambiguity around bulk substances

That gives risk teams something concrete to work with.

2. Reduced Reliance on RUO Labeling

As peptides move into clearer frameworks through 2026 review cycles, merchants can move away from pretending customers are researchers.

That removes one of the biggest friction points in underwriting.

3. Product-Market Alignment Improves

When product structure, customer behavior, and marketing language align, approval rates increase and shutdown risk drops.

That alignment has been missing. It starts to come back as regulation catches up.

What Payment Processors Will Do Next

Processors are not going to open access overnight.

They will move in phases tied to regulatory clarity through late 2026 and into 2027:

Phase 1: Selective Acceptance (Around July 2026 Reviews)

- established operators

- clean branding and disclosures

- conservative positioning

Phase 2: Tight Monitoring (As Reviews Progress)

- strict chargeback thresholds

- fulfillment scrutiny

- ongoing marketing review

Phase 3: Category Normalization (Post-Review Outcomes)

- more banks enter

- pricing stabilizes

- reserve requirements ease

Most merchants will not make it to Phase 3 because they are not built for this level of scrutiny.

Where Most Peptide Sellers Will Fail

Most peptide companies are not prepared for real underwriting.

Common issues:

- no compliance documentation

- unclear supply chain transparency

- marketing that implies medical outcomes

- subscription models that increase disputes

- checkout flows that trigger card network alerts

These problems require structural fixes, not patches.

The Opportunity: Owning the Payment Layer

If you treat payments as an afterthought, you lose leverage.

If you control the payment strategy, you create stability.

A processor that understands:

- peptide-specific risk signals

- the RUO transition problem

- SKU-level underwriting logic

- behavioral fraud versus legitimate demand

has an edge.

Approval is one step. Longevity is what matters.

What a Real Peptide Payment Solution Looks Like

A serious processor in this space should provide:

- pre-underwriting based on product structure

- guidance on SKU design and packaging signals

- checkout optimization to reduce flags

- descriptor strategy to reduce disputes

- bank relationships aligned with the regulatory shift unfolding through 2026

Anything less leads to instability.

Bottom Line

The peptide market is moving out of regulatory chaos.

Starting in July 2026, that shift becomes formal.

Payments will follow.

This transition will filter the market:

- weak operators get removed

- unprepared processors get exposed

- structured businesses gain ground

If you are still relying on RUO positioning and hoping your processor ignores it, your timeline is limited.

The window is opening.

Positioning determines who makes it through.